Blog

Factor Insights - Q3 2023

Factor Insights – The vexation of value

After a decade of lousy relative performance, value has entered an environment that is close to its sweet spot. Environments characterized by high and rising interest rates, elevated inflation, and strong economic growth tend to be ideal for value. But macro headwinds have thrown a wrench in some of these general relationships, leading to a rough start to the year for value in general.

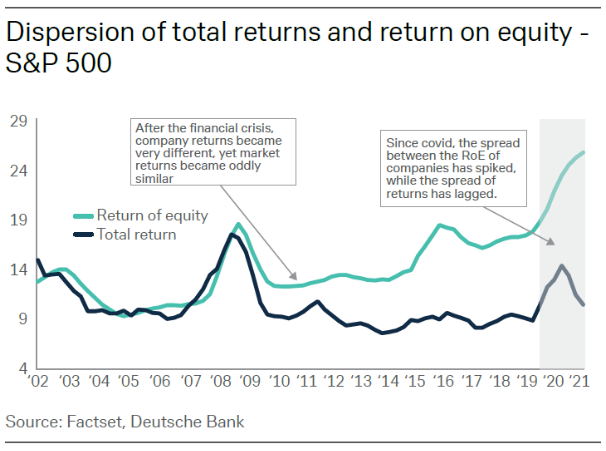

Value underperformance prior to 2022 had several underlying causes. Technology and other growthier names, which can be thought of as anti-value, were on a tear. Low rates meant risk-seekers were able to deploy inexpensive capital to chase long-term growth that appeared cheap when discounted to present day. Concurrently, a significant amount of capital poured into equity markets, as investors sought a return that was unavailable in safer investments, often referred to as the “there-is-no-alternative (or TINA)” trade. As noted by Luke Templeman of Deutsche Bank1, much of that capital flowed to market capitalization-weighted index funds. As seen in the chart here, demand for these funds likely contributed to the stock prices of their constituents moving together, regardless of their fundamental characteristics. The rising tide lifted all boats, but many growth stocks also rode the bigger multiple-expansion waves.

Fortunes turned in 2022, as rates and inflation rose throughout the year, and value went on to lead growth by a healthy margin. The MSCI USA Enhanced Value index bested the MSCI USA Growth index by almost 18% in 2022. However, year-to-date through June 30, 2023, that relationship is reversed, with the value index giving up all its relative gains against growth from last year. Inflation remains high and rates are still elevated, so what gives?

One element may be the market cycle. Leading indicators from the housing, manufacturing, and credit sectors suggest the U.S. is in the late expansion stage of the economic cycle2. Research by QRG Capital Management shows that value tends to lag when the economy enters the last hurrah of this stage, whereas growth stocks continue the market’s upward momentum, sometimes with unjustified exuberance3. They note, however, that pursuing concentrated investment in growth stocks at this late stage in the expansion should be done with care, as the performance of value stocks sharply reverses during recessions. Citing elevated inflation, high interest rates, and a cooling labor market, the Conference Board4 expects consumer spending to moderate, after acting as a tailwind in the first quarter, along with a continued slowdown in business investment in the U.S. As a result, the group forecasts a domestic recession in the second half of this year and expects it will bleed into 2024.

As investors position for this slower growth, they have also been buying up quality stocks. The quality factor has tended to have a positive correlation with the growth style, as stocks in this style generally have solid balance sheets. This effect has played out this year particularly within the technology sector, where a handful of high-quality mega cap names, including Amazon, Meta, and Tesla, have been hefty drivers of overall equity returns in the U.S. to the detriment of diversified and value investors alike.

Further, while rates remain relatively high overall, they have shifted down marginally across the curve. The 10-year Treasury started the year around 3.75% and ended June around 3.6% after hitting a low of 3.3% in May. While slight, these lower rates may have acted as a propellant to reprice growth stocks at the expense of value.

Another contributor may be simple rebalancing of portfolios after tax lost harvesting at the end of 2022. Underperforming names that were sold during the harvesting season were likely to be disproportionately from the growth camp. As a result, swaths of portfolios likely had to rebalance to targets after expiration of the wash sale window at the beginning of the year. A disproportionate amount of growth’s returns so far this year were earned in January, perhaps stemming from this tide of demand.

Over the very long-term, the value premium has been a consistent component of excess return. However, the volatility of its performance over the last 20 years is much higher than the historical experience, and reversals between growth and value leadership have become more frequent5. The economic regime of cheap capital and low inflation have certainly been a headwind for this factor. Going forward, the relative performance of value will likely depend on to what extent the current macro regime is secular rather than cyclical. While it is unlikely that we will see a shift toward 1970s-style inflation, hurdles exist that may result in higher-than-target rates and inflation that are not transitory but persistent. Demographic changes reflect aging populations and lower birth rates, which suggests that labor will not be as plentiful as it was during the last several decades. The result may be a spike in labor costs. Growing pains (and associated costs) are likely as economies transition away from a carbon-based economy to something more sustainable, which could further fuel inflation and central bank rate hikes in response. However, cyclical factors may still cause shorter term style rotations between growth and value, even during broader secular shifts. The year-to-date period may prove to be a textbook example.

Sources:

1Templeman, Luke. The end of free money in stock markets. 8 December, 2021. Available at https://www.dbresearch.com/PROD/RPS_EN-PROD/PROD0000000000520992/7__The_end_of_free_money_in_stock_markets.xhtml;

2Fidelity Investments. Economic indicators hint at a coming slowdown. May, 2023. Available at https://www.fidelity.com/learning-center/trading-investing/markets-sectors/business-cycle-update#:~:text=The%20US%20is%20in%20the,the%20second%20half%20of%202023.

3Zvingelis, Janis. Factor Performance and the Market Cycle. QRG Capital Management. 24 May 2021.

4The Conference Board Economic Forecast for the US Economy. 10 May, 2023. Available at https://www.conference-board.org/research/us-forecast

5Northern Trust. Factor Research Quarterly. Investing in Value without Betting Against Growth. Presented July 12, 2023.

Past performance is not indicative of future results. The information, analysis and opinions expressed herein are for informational purposes only and do not necessarily reflect the views of Envestnet. These views reflect the judgment of the author as of the date of writing and are subject to change at any time without notice. Nothing contained in this piece is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.