Commentaries

Factor Insights - Q3 2022

Lost in translation

A sign translated to English at a zoo in Budapest reads, “Please do not feed the animals. If you have any suitable food, give it to the guard on duty.” Mercedes Benz’s name was translated in China to “Bensi”, meaning “rush to die”. The American Dairy Association’s “Got milk?” slogan translated to mean “Are you lactating?” in Spanish-speaking countries. However unintentional, important context is lost in translation every day. The same might be at risk in the leap from academic theory to real-world implementation in any discipline. Case in point, factor-based investing earned its stripes when theorists began creating long-short factors for study in an academic setting. But in many cases, real-world portfolio management is restricted by limitations on short selling. Is it possible that the factor-based investment approach has lost some (probably less comical) context with its jump from theory to practice?

The long and long-short of harvesting risk premia

Like any good portfolio management technique, factor-based investing started as the brainchild of academics. Ken French and Eugene Fama pioneered the field with their hypothesis that risk factors beyond the market risk premium were at play in determining asset prices and expected returns. They tested this theory by constructing long-short portfolios targeting specific factors, like value, momentum, and small size. In their value portfolio for example, long positions in low price/book stocks were offset by short positions in high price/book stocks, resulting in a portfolio that favored value stocks and stripped out the effect of the market. In a similar vein, a long-only factor product could be combined with derivatives to hedge market risk, resulting in a profile akin to the long-short theory. These construction methods make for digestible quantitative assessments, and they are readily accessible to institutions and other qualified investors in real-world implementation. However, these options are not always practical or implementable for retail investors. As a result, long-only exchange traded products and managed accounts have emerged to fill that void.

Long-only products are constructed to benefit from factor premia by tilting their portfolios to overweight stocks with higher exposure to desired factors, and underweighting stocks with low exposures. These products are often broadly diversified to reduce stock specific risk and can be managed to pick up factor premia within tracking error constraints relative to broad market capitalization-weighted benchmarks without using leverage or derivatives.

But while market risk is of little concern for long-short portfolios, it is a primary driver of performance for long-only factor products. The restriction on short sales in these portfolios means that at best they can underweight securities or not hold them at all, but the underweight allocation is redeployed to overweight other securities. The net result is that performance of the long-only portfolios is dominated by market risk exposure, with market betas generally near one, though positive betas to other risk factors ensures some tracking error and excess return potential versus market cap-weighted indices. They essentially become a one-stop shop to capture both market and style factor risk premia.

Know what you own

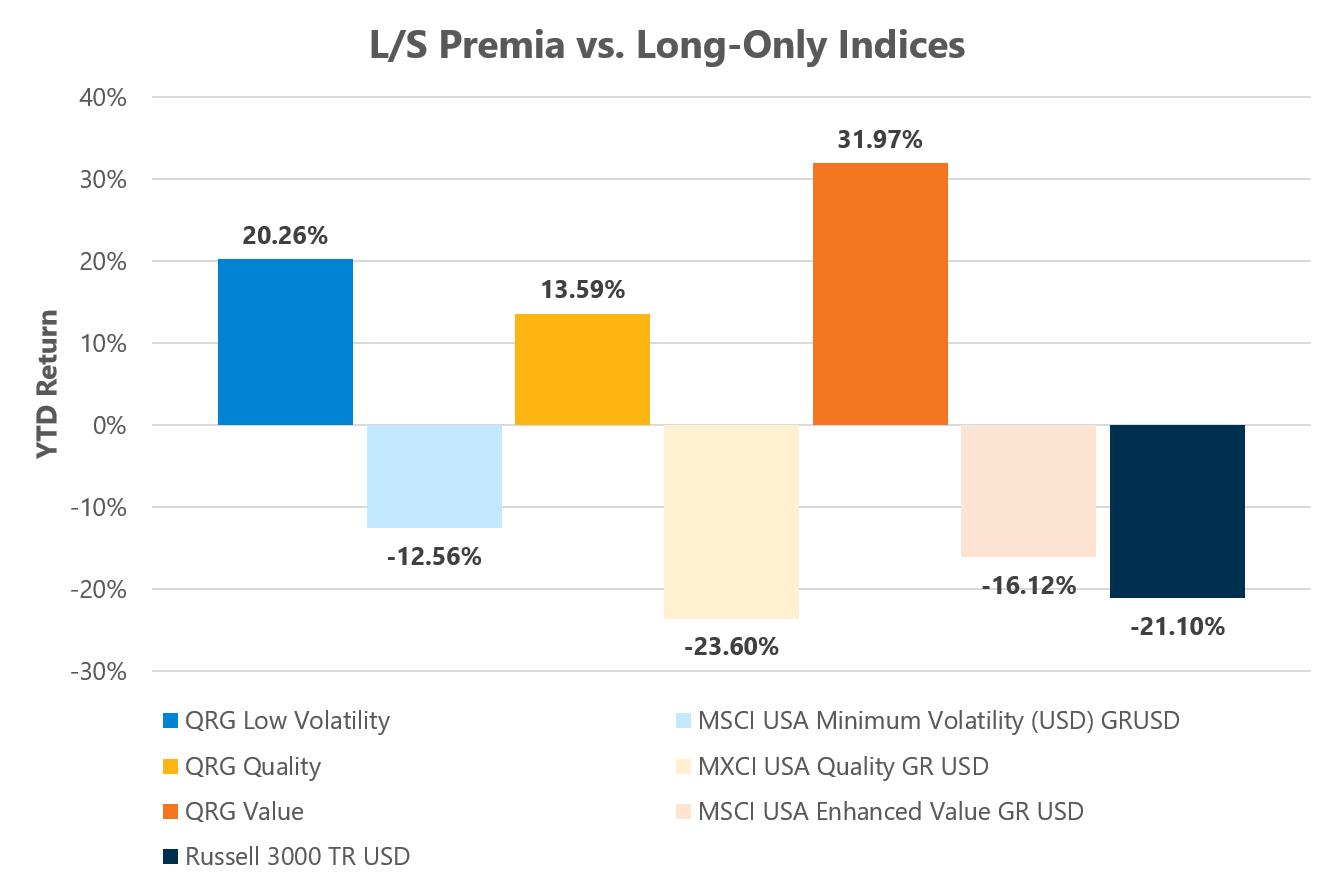

Performance results between the long-short risk premia and long-only factor tilted portfolios will vary widely because of the market risk component. To illustrate this, the chart below shows near-term performance of the long-short minimum volatility, quality and value risk premia calculated by Envestnet’s QRG Capital Management team compared to representative long-only indices through June 30, 2022. The impact of exposure to market risk is clear in the long-only context, and performance of the quality premia versus the long-only quality index underscores the point. The quality premia itself was positive, as expected in such a risk-off environment, and mirrors the long-term observation that low quality stocks lag their higher quality counterparts. However, the long-only quality index underperformed the broad market. At least part of this underperformance could be attributed to the broad-based tech sell-off in the equity market. Although the technology sector generally has favorable quality characteristics, higher quality tech names have of late sold off alongside more speculative issues in a rotation away from interest-rate sensitive sectors.

Source: Morningstar Direct, Envestnet. As of 6.30.2022

Superiority complex

The merits of both the long-short and long-only approach to capturing factor premia have been analyzed through various research studies, and both have their uses. Blitz, Baltussen and van Vilet (2020) argue that most added value from factor premia comes from the long positions in a long-short portfolio, the long portion offers more diversification than the short portion, and the performance of the short portfolio is subsumed by the long portfolio.1 Long-short approaches offer their own benefits however, and an AQR report concluded that long-short approaches can provide better diversification to portfolios that are already heavily exposed to market risk premia and can more efficiently capture factor premia.2 A working research paper from Briere and Ariane suggests that even constrained short-selling, in a 130/30 portfolio for example, enhances the performance of factor-investing.3 They showed that the frontier associated with long-only factors dominates the market-capitalization frontier, but that the long-only frontier is itself dominated by the original long/short Fama-French frontier and other implementations that allow for long-short factor construction.

From a qualitative perspective, long-only implementations may have the upper hand. For example, institutions and retail investors alike may appreciate the lower tracking error to traditional benchmarks. Additionally, fees for long-only products tend to be lower because they are dominated by market beta, and don’t have the additional operational complexity involved with shorting securities.

All is not lost

Although factor-based investing started with a long-short thesis, not all is lost in translation to long-only implementation. Both long-short and long-only versions of factor investing gain clients exposure to fundamental sources of return, and both can play a part in client portfolios. Long-only products may be suitable in the core or traditional asset class sleeve, while long-short or long-only plus derivatives may fit as a higher tracking error approach to capturing purer premia within an alternatives sleeve.

Whatever the approach, it is important to bear in mind performance implications. Long-only portfolios will be heavily affected by market performance, while long-short portfolios will feel much less of the market impact but will have their own ups and downs along with the cyclicality of factor premia (a case for diversification of factor exposure best made in another blog post). Whatever implementation is chosen, the research is clear that over the long-run, overexposure to these rewarded risk premia has the potential to harvest risk-adjusted outperformance of market capitalization-weighted indices.

Sources:

1. Blitz, David, Guido Baltussen, Pim Van Vliet. “When Equity Factors Drop Their Shorts,” Financial Analysts Journal, 2020, 76(4):73-99. Accessed at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3493305

2. Ilmanen, Antti, Ronen Israel, Dan Villalon. “Style Investing: The Long and Long/Short of It,” Accessed at https://www.aqr.com/-/media/AQR/Documents/Insights/Trade-Publications/Style-Investing-The-Long-and-the-Long-Short-of-It.pdf

3. Briere, Marie, Ariane Szafarz. “Factor Investing: The Rocky Road from Long-Only to Long-Short,” Amundi Asset Management working paper. April, 2017.

Past performance is not indicative of future results. The information, analysis and opinions expressed herein are for informational purposes only and do not necessarily reflect the views of Envestnet. These views reflect the judgment of the author as of the date of writing and are subject to change at any time without notice. Nothing contained in this piece is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.