Commentaries

Factor Insights - Q4 2022

Diversify your factors too

A key idea behind factor-based investing is that factor risks are rewarded because they cannot be diversified away, whereas as security-specific risks are not rewarded for precisely the opposite reason. It’s the same case that is made for diversifying broad asset classes like stocks and bonds and sub-asset classes like sectors and issuers. In addition, like all of these investment categories, factor premia are cyclical, and the best way to deal with the cyclicality of individual factor returns is to diversify exposure to them.

A familiar case for diversification

The benefits of diversification stem from less than perfect correlation among assets. One zigs and the other zags, and voila – a reduction in volatility with a less than one-for-one reduction in return. The broadly accepted risk factors of value, quality, small size, low volatility and momentum are each formulated to capture a specific equity characteristic. Though those characteristics may be related, they are less than perfectly correlated.

Exhibit 1 shows correlations for domestic factor premia as calculated by QRG Capital Management over the last 20 years. Most factor correlations are negative, indicating that they tend to move in opposite directions. The highest correlation is between the quality and low volatility factors, and the lowest correlation is between quality and size. In addition to low correlation with each other, these factors also have low or negative correlation to the broad market as measured by the MSCI USA index, suggesting they serve to diversify broad market exposure as well.

Exhibit 1: Factors tend not to move together over long periods

Source: QRG Capital Management, Morningstar Direct. Trailing 20 years. Data as of 9/30/22.

While the returns shown in exhibit 1 are for long-short factor premia, most retail investors access factors through long-only products in practice, which introduces market factor exposure to the portfolio. Because these long-only portfolios are dominated by this common influence, it’s unlikely that pairing long-only factor portfolios will lead to a meaningful reduction in total portfolio risk in any period. However, exhibit 1 can also be thought of as the excess return correlations among the various factors, and because they are low or negative, combining them results in a significant reduction in active risk relative to investing in individual factors.

Factor premia and the economic environment

The source of these less than perfect correlations comes from the fact that factors are cyclical, and generally perform differently across market environments. Fluctuations in economic activity are incredibly difficult to predict and time, but they affect factor performance just the same.

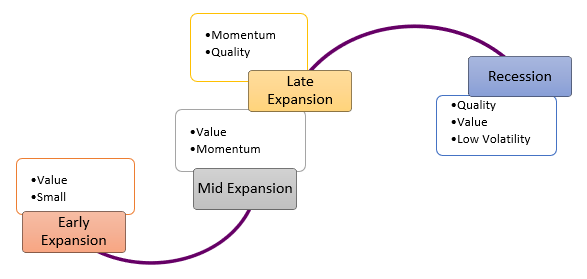

Exhibit 2 notes which factors tend to perform well in each phase of the market cycle. Small caps tend to do well as investors start to seek risky assets again post-recession and into expansion. During expansionary phases, trending markets bode well for the momentum factor and value stocks are sought after for their return potential. Before recession sets in, investors become cautious and seek high quality stocks, while in recession, safety is key and low volatility is also in vogue.

Exhibit 2: Factors perform differently across the economic cycle

The regime-dependency of factor returns makes timing allocations to them tempting. But these general relationships are not guaranteed, and in fact have endured short-term periods where correlations have completely reversed from long-term relationships or factor performance was misaligned with expectations. Value add from factor-timing is far from guaranteed.

Multifactor portfolio performance

The risk of these reversals along with the low correlation of these factors suggest most investors are better off diversifying their factor allocations and seeking to capture their premia over the long term. Exhibit 3 below shows risk and return characteristics for several long-only factor indices, as well as characteristics for an equally-weighted portfolio of these indices, over the last 20 years.

Exhibit 3: Single factors are more volatile than a blend

|

Trailing 20 Years |

Return |

Std Dev |

Tracking Error |

Excess Return |

Sharpe Ratio |

Information Ratio |

Beta |

Worst Quarter |

Max Drawdown |

|

MSCI USA Enhanced Value |

9.31 |

17.38 |

6.08 |

0.17 |

0.53 |

0.03 |

1.09 |

-29.19 |

-54.96 |

|

MSCI USA Quality |

10.23 |

13.85 |

3.64 |

1.09 |

0.69 |

0.28 |

0.90 |

-18.24 |

-40.49 |

|

MSCI USA Momentum |

10.13 |

15.48 |

7.31 |

0.99 |

0.62 |

0.12 |

0.92 |

-23.83 |

-51.72 |

|

MSCI USA Small Cap |

9.46 |

19.35 |

8.24 |

0.32 |

0.50 |

0.04 |

1.19 |

-31.26 |

-54.00 |

|

MSCI USA Min Volatility |

9.28 |

11.85 |

6.07 |

0.14 |

0.71 |

0.02 |

0.73 |

-18.92 |

-40.98 |

|

Equal Weighted Multifactor Portfolio |

9.88 |

14.66 |

2.61 |

0.74 |

0.63 |

0.26 |

0.97 |

-21.66 |

-47.78 |

|

MSCI USA |

9.14 |

14.95 |

-- |

-- |

0.58 |

-- |

-- |

-22.22 |

-50.65 |

Source: Morningstar Direct, MSCI Inc.

Data as of 9/30/22

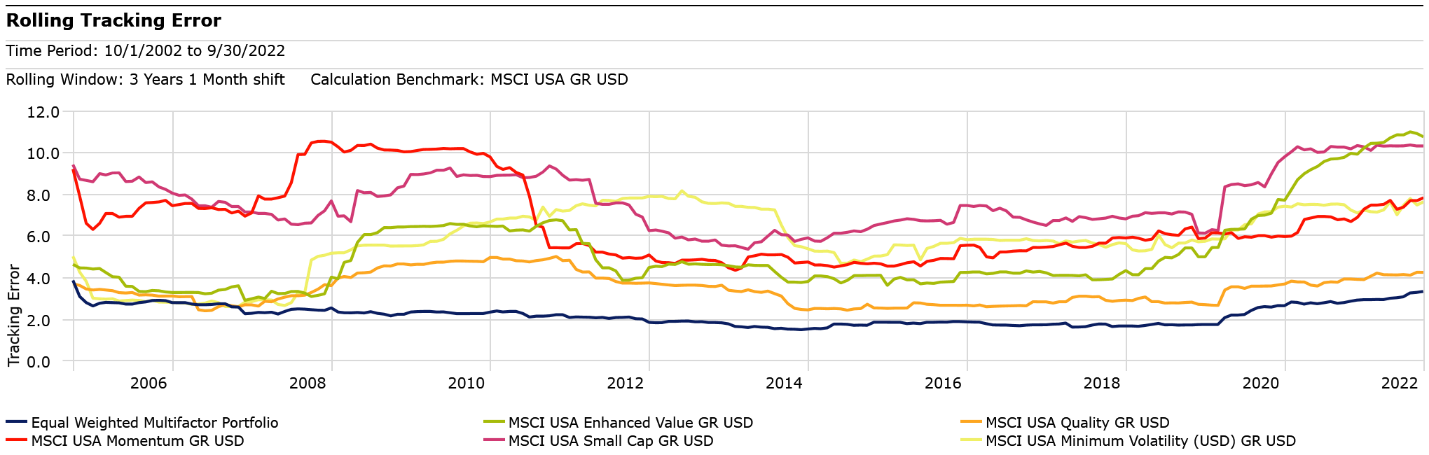

From a risk-adjusted performance perspective, the Sharpe ratio of the blended portfolio improves over the average Sharpe ratio of all the single factor indices. Further, its information ratio, which measures performance relative to the MSCI USA index in this case rather than the risk-free rate as in the Sharpe ratio, is more attractive than almost all of the single factor indices. This is because of the lower tracking error (also known as active risk) of the multi factor portfolio. As noted previously, total risk measured by standard deviation does not vastly improve relative to the average of the underlying single factor indices. However, tracking error is much improved relative to the average of the indices and more consistent as well, as seen in exhibit 4.

Exhibit 4: The multifactor portfolio had consistently lower active risk

Source: Morningstar Direct, MSCI Inc

Into practice

Overall, the multifactor portfolio proxied here produced more consistent excess risk-adjusted returns with similar or better downside than individual factors because of the benefits of diversification. Factors can be combined in a number of ways beyond simple equal-weighting, and there is good reason to develop a thoughtful and proactive weighting approach. Whatever that approach may be, factor diversification is the most straightforward way to seek excess return from factors in a risk-aware manner.

Past performance is not indicative of future results. The information, analysis and opinions expressed herein are for informational purposes only and do not necessarily reflect the views of Envestnet. These views reflect the judgment of the author as of the date of writing and are subject to change at any time without notice. Nothing contained in this piece is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.