Commentaries

What We are Hearing and Seeing 11/17/22

What We are Hearing and Seeing – November 17, 2022

Tactical Strategies Remain Out of Favor

By Brooks Friederich

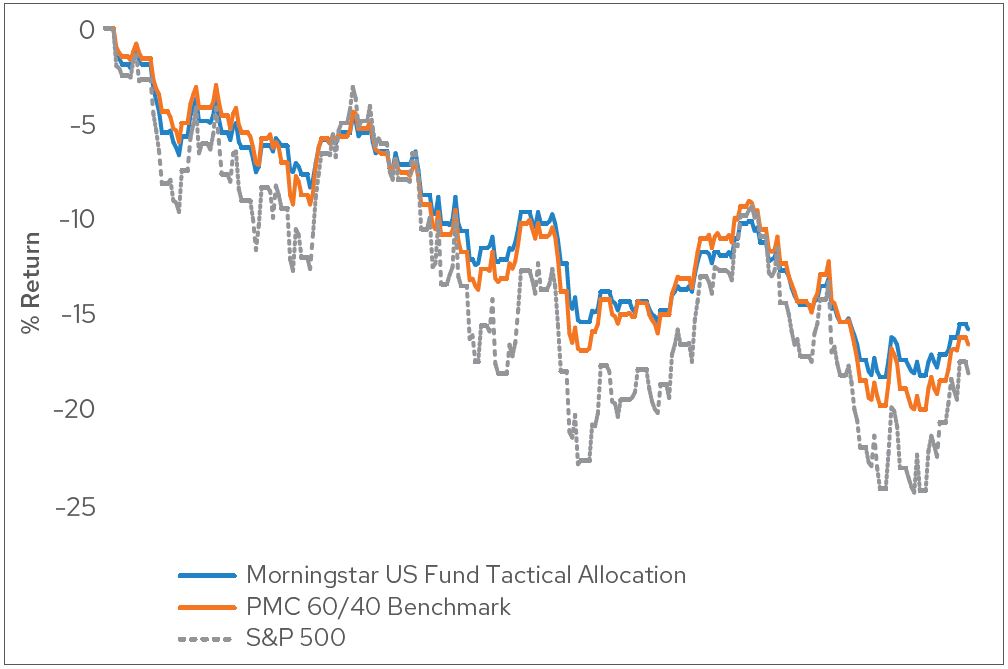

Like many investment styles, tactical asset allocation strategies have experienced many in-favor and out- of-favor periods. During the depths of the Great Financial Crisis (GFC), highly flexible, tactical strategies were some of the more popular investment strategies utilized by financial advisors. Most of these tactical strategies implement rules-based, quantitative models that shift assets to defensive securities (i.e., cash, money market securities, and short-term bonds) during periods of market stress—doing their best to “win by not losing.” Tactical allocation strategies then aim to add equity risk when the markets seem poised to recover.

Fast forward to 2022 where we have experienced a volatile market environment that has produced double-digit negative absolute returns across most asset classes. At Envestnet | PMC, though, we have not experienced the demand for tactical strategies from financial advisors like we did back during the GFC. Leveraging Envestnet’s internal data and analytics, we find that tactical model portfolios have accounted for approximately 5% of asset inflows into model portfolios over the past year. Through the end of October, a diversified 60/40 benchmark was down around 16%, a similar return to that of Morningstar’s Tactical Allocation peer group with similar drawdown profiles.

Tactical strategies can serve a place in a portfolio (typically as a satellite component), but through the lens of our research and due diligence, they have had difficulty in delivering consistent superior long-term investment results. Over the long-term, most tactical strategies generate similar risk-return results to a diversified 60/40 asset allocation. We commend financial advisors for continuing to stick to managing diversified portfolios, helping to coach their clients through market events, and focusing on longer-term financial goals and investment objectives. In today’s market environment, tactical asset allocation strategies seem unlikely to be a critical element of most portfolios, though.

Chart Source

Source: Morningstar Direct. Envestnet | PMC.

EM Debt: Headwinds Remain, but Opportunities Beginning to Surface

By Navaneeth Krishnan

It has been a tough year so far for emerging market (EM) bond investors as high inflation, rising developed market interest rates, elevated geopolitical risks, and a strong US dollar have weighed down the asset class. All segments of the EM debt (EMD) market have been impacted; rising US Treasury yields have hurt both corporate and sovereign bonds denominated in hard currencies, and a relentless rally in the US dollar has been a drag on local currency bonds. Similarly, all three indices within the EMD spectrum, which separately represent each of these categories, have meaningfully underperformed the Bloomberg US Aggregate Bond Index (2-9% underperformance depending on sector). Given this backdrop, investors continue to rotate away from EMD, evidenced by both Morningstar EMD categories (Emerging Markets Bond and Emerging-Markets Local-Currency Bond) having seen their total net assets drop by roughly 30% on a year-to-date basis.

While the broader backdrop continues to be challenging, the managers we cover in this space have started to become more optimistic about this asset class. While acknowledging the presence of exogenous and idiosyncratic risks, EMD continues to offer a substantial yield premium, and EM focused managers believe that EMD looks compelling from a long-term risk-reward perspective relative to other credit sectors. Additionally, market volatility has increased valuation dispersion within the EMD space, thus creating sector and security selection opportunities for active managers. Any uptick in demand would also skew technical factors positively in an asset class that has seen net negative new bond issuance so far this year. On a year-to-date basis, as of September 30, EM sovereign and corporate issuance combined stands at around $270B versus $670B in 2021.1

Even though valuations are compelling and technicals could quickly become favorable, it might still be too early to call a market bottom. The macro backdrop remains challenging as global central banks continue to embark on their tightening journey to suppress elevated inflation levels. Furthermore, although Russia is no longer part of the EM indices, its ongoing assault on Ukraine continues to strain the global economy, thus elevating idiosyncratic risks among weaker EM and frontier issuers. China also remains an uncertainty, as the nation’s property sector slowdown and COVID restrictions continue to put pressure on Chinese, and thus Asian corporate issuers. Finally, Latin America continues to navigate political risks despite benefiting from higher commodity prices. While most of the aforementioned risks are part-and-parcel of EMD investing, they suggest country and issuer selection will be paramount for the foreseeable future. This concept underscores the importance of an actively managed approach to the asset class.

1 https://www.ft.com/content/4b8f49ba-58d3-4e8e-a06b-a6eaa940d79b (Emerging market bond slump creates opportunities for investors – FT)

Know What You Own

By Ling-Wei Hew, CFA

When year-to-date US equity sector returns range anywhere from -36.45% to 65.91%, portfolio managers continue to remind investors about the importance of knowing what they own and staying invested for the long-term. By not doing so, investors may react to short-term dispersions in sector performance and inadvertently participate in a sector timing strategy. This situation has a myriad of implications throughout investing but was especially important in 2022 for ESG portfolios that looked to capture broad market exposure through ETFs or indexed products.

We can explore this concept by using the MSCI USA Index, a popular choice for ETFs looking to replicate broad market exposure to the domestic equity market, as an example. There are several ESG flavors of this parent index, including the MSCI USA ESG Focus Index, MSCI USA Choice ESG Screened Index, and the MSCI USA ESG Universal Index. Each of these flavors has its own unique methodology and approach to capturing ESG factors that may lead to significant differences in the composition of the underlying constituents. Highlighting some of the best and worst performing sectors of the market in the table below, we can examine how different ESG methodologies can lead to significant sector biases and the impact that this has on performance. If we take a look at the MSCI USA Choice Screened Index, as an example, we can see that a large overweight to information technology, one of the worst performing sectors, and an underweight to energy, one of the best performing sectors, led the index to significantly underperform the MSCI USA Index.

These unintended biases are not unique to ESG indexes and can often be seen across index providers that replicate common exposures, such as the domestic small cap and emerging market equity universes. Furthermore, these biases do not occur only among sectors, but can also occur among other dimensions such as factors, styles, countries, and sub-asset classes. The market volatility has been unkind to most, but it always serves as a good reminder to stay invested and know what you own.

UK Economy – Uncertain Winter Ahead

By Ramasubramaniam P. CFA

The Bank of England (BoE) on Thursday raised interest rate by 0.75% to 3%, its single biggest rate hike in 33 years, to dampen the skyrocketing inflation that is at a 40 year high. However, the challenge to the economy is multifaceted, as rate hikes this year have probably pushed the country into a recession, leading the BoE to warn that the this could be the longest recession on record. However, the Monetary Policy Committee hinted that the peak rate may be lower than what is currently priced into financial markets.

Many of the asset managers we speak with point out that the UK’s problems are not recent. Since the global financial crisis, Britain’s GDP per capita has grown at just 0.5% a year, compared with an average 2% between 1971 and 2007. Recently, three macro events have added to the woes of the economy. First, Brexit cut trade flows, inward migration, and most likely depressed the level of GDP permanently. Second, the COVID-19 pandemic led to supply chain disruptions, a reduction in the labor force, and the government’s expansionary fiscal response took a toll on the exchequer (the UK treasury). Third, the Russia-Ukraine crisis has driven up energy prices and diminished household real incomes.

The challenges facing new PM Rishi Sunak are manifold. The Truss-Kwarteng Energy Price Guarantee exposed some difficult tradeoffs. The planned expansion would have tampered rising inflation but would have aggravated the high interest rate scenario. For an economy riding a debt-funded housing boom, the resulting increase in debt servicing costs for the household sector would have been disastrous. Analysts estimate that high interest rates would also lead to double digit declines in housing prices. For the year 2023, managers are estimating that the UK economy will likely contract by about 0.5%. However, a strong medium-term fiscal plan by the government would reassure financial markets. Given heightened risks

of a recession, energy price uncertainty, and a potentially stagflationary economy, most non-US equity managers are underweight UK stocks while selectively looking for defensive companies with higher near- term earnings certainty or those that can pass inflationary pressures through to their buyers. They also favor UK-domiciled multinationals that are less impacted by the domestic economy.

How Does a Large Cap Value Manager Think in a Bear Market?

By David Chandler, CFA

It has certainly been an interesting trailing twelve months to say the least. At roughly this time last year (November 2021), the market was debating whether to believe the Fed that inflation was transitory. That debate has now shifted to whether the Fed will drive us into a severe recession or merely a moderate one in its fight to bring the so called “transitory” inflation back under control. The good old days of rising markets and “free” money now seem long gone.

Given this new monetary policy regime and current bear market, we felt it would be useful to report on what our large cap value (LCV) managers are thinking. The following update is based on commentary from LCV managers under PMC’s research coverage and reflects their views at the end of Q3 2022. Certainly, there is divergence of opinion within the group—it’s what makes a market after all—but we think this summary is representative of some consensus views within the asset class on a handful of topics and sectors:

Macroeconomic Environment

Most LCV managers believe the recession we are in (or likely will be in, depending on your point of view) will be a moderate one, not a “soft landing” but also not a disaster. The thinking is it will be at its worst during Q4 2022 and Q1 2023. After that, they expect the market and economy will adjust to this “new normal” of tight monetary policy and modestly elevated inflation (4-5% CPI). Expectations are that it will take much longer for the Fed to get inflation back down to its 2% target.

Value vs. Growth

Unsurprisingly, the group thinks now is the time for value to close the gap in performance with growth. Of course, they’ve been calling for that to happen for years now, and no managers have ever said it’s a bad time for their strategy. Putting that aside, they do point out that the valuation gap between LCV and LCG remain at historically high levels. Being the “reversion to the mean” crowd that they are, they ultimately think the gap will close at some point. In many ways, growth stocks are analogous to zero coupon bonds. It is therefore not surprising that they’ve suffered proportionally more in this bear market. LCV managers also point out that the asset class has tended to outperform in similar past environments.

Energy

Oil prices are likely to remain high. The sector should continue to report strong financial results, and the bull market in this sector might very well continue. Oil and natural gas supplies remain restricted, particularly in Europe due to the ongoing Russia/Ukraine conflict. The recent OPEC production cut only exacerbates the situation. Furthermore, exploration has fallen off in recent years as companies diverted

capital into renewable projects. New reserves were barely keeping up with production in recent years, and that was before all the COVID shutdowns. Now that demand has normalized, it will be some time before supply catches up.

Financials

Banks should do better than the overall market currently expects. They are presently trading at recession level multiples, but large cap banks have much better capital ratios than they typically do going into recessions. They are certainly in a much better position as a group than in 2008. Also, higher rates should help them to the extent many have low-cost funds that they can now lend out at much higher rates.

Healthcare

Of the traditionally defensive sectors, it’s interesting that Healthcare is perhaps the only one that LCV managers all agree on being attractive. Managed care firms are still suffering from COVID

underutilization, and their valuations remain low. The thinking is there is still a backlog of COVID deferred medical procedures which can’t be deferred forever. Many procedures will proceed despite a recession. Better utilization of facilities should result in better financial results and should eventually be rewarded by the market.

Communication Services

Q3 was a very bad quarter for LCV favorites Verizon, AT&T, and Comcast. They all declined by around

25% in the face of intense competition. The deployment of 5G networks should help the industry over the long-term. However, in the near-term, 5G is dramatically increasing the supply of bandwidth without a concurrent surge in bandwidth demand. Unsurprisingly, the industry is competitively lowering data pricing down to marginal cost, which is close to zero. This situation should normalize as applications catch up to the technology, but the Q3 decline has made the valuations of these stocks compelling.

Consumer Staples

Many, excepting some of the dividend-oriented managers, view this traditionally defensive sector as significantly overvalued given generally slow growth and high valuations. Some have held this view for years. An ongoing debate over the last decade or so is whether many of these firms have lost their pricing power. Store brands are higher quality and more prevalent than when inflation was last this high in the 1970s. There is some speculation that consumers will trade down from name brands as inflation takes away their discretionary spending power. This might not be the case for something like Coca-Cola, where taste probably factors as much as price, but it could be true for products where price is a more dominant part of the buying decision.

The information, analysis, and opinions expressed herein are for general and educational purposes only. Nothing contained in this brochure is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. All investments carry a certain risk, and there is no assurance that an investment will provide positive performance over any period of time. An investor may experience loss of principal. The asset classes and/or investment strategies described may not be suitable for all investors and investors should consult with an investment advisor to determine the appropriate investment strategy. Investment decisions should always be made based on the investor’s specific financial needs and objectives, goals, time horizon and risk tolerance. Past performance is not indicative of future results.

This material is not meant as a recommendation or endorsement of any specific security or strategy. Information has been obtained from sources believed to be reliable, however, Envestnet | PMC cannot guarantee the accuracy of the information provided. The information, analysis and opinions expressed herein reflect our judgment as of the date of writing and are subject to change at any time without notice. An individual’s situation may vary; therefore, the information provided above should be relied upon only when coordinated with individual professional advice. Reliance upon any information is at the individual’s sole discretion. Diversification does not guarantee profit or protect against loss in declining markets.

FOR INVESTMENT PROFESSIONAL USE ONLY

© 2022 Envestnet. All rights reserved.