Commentaries

PMC Market Commentary: May 30, 2014

A Macro View – Factor-Tilted Portfolios

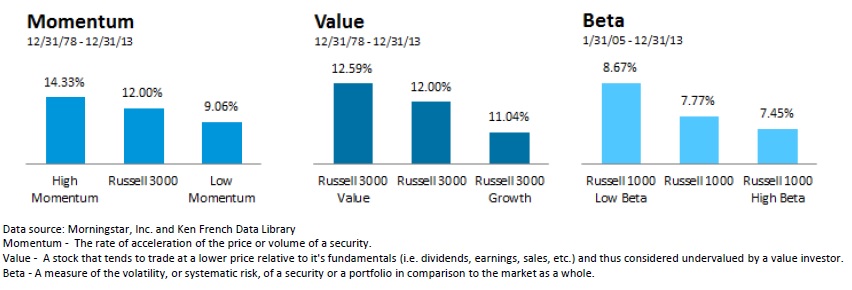

Over the past couple of decades there has been a significant amount of academic and industry research focused on identifying the primary drivers, or factors, determining equity price movements. Professors Eugene Fama and Kenneth French built on earlier research by others in setting forth their famous three-factor model of stock prices in 1993. Fama and French identified three factors – exposures to the market, size (small caps) and value – as being three key drivers that provide anomalous excess returns over time. The size factor holds that in general, smaller cap stocks outperform large cap issues. The value factor thesis is that stocks that exhibit more favorable valuations – such as those having higher Book Value/Price ratios – tend to outperform stocks that are perceived to be more richly valued.

The Fama-French findings have since spurred additional research attempting to better understand factors resulting in superior excess returns. Mark Carhart introduced the momentum factor in 1997. He showed that stocks that have performed well over the past tend to continue to perform well for a period of time. Specifically, he looked at performance over the past 12 months as being an indicator of performance over the next month. Along with value, momentum has been shown to be pervasive in most asset classes. The momentum factor is often included with the original Fama-French factors in a “four-factor model.”

Other market premia that researchers have identified include liquidity (i.e., stocks with lower liquidity outperform more highly liquid names); quality (i.e., higher quality outperforms lower quality); and defensive (i.e., lower beta stocks outperform higher beta names).

Various theories have been posited as to why these asset pricing anomalies are experienced. Since the efficient market hypothesis holds that all information is contained in stock prices, and that no such premia are exploitable, academics have suggested that behavioral issues are the likely explanation.

A significant implication of this research is that exposure to these factors is increasingly being made available in a portfolio context. Investment managers are able to construct portfolios that have “tilts” toward one or more of these factors in an effort to outperform the benchmark. In the mutual fund world, Dimensional Fund Advisors (DFA) and AQR Capital Management have been at the forefront of the research and implementation of such strategies. In terms of separate accounts, PMC will be building upon its recent introduction of Quantitative Portfolios by introducing factor-tilted versions of the QPs. Finally, there are also several factor-tilted indices with associated exchange-traded funds (ETFs).

The information, analysis, and opinions expressed herein are for general and educational purposes only. Nothing contained in this weekly review is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. All investments carry a certain risk, and there is no assurance that an investment will provide positive performance over any period of time. An investor may experience loss of principal. Investment decisions should always be made based on the investor’s specific financial needs and objectives, goals, time horizon, and risk tolerance. The asset classes and/or investment strategies described may not be suitable for all investors and investors should consult with an investment advisor to determine the appropriate investment strategy. Past performance is not indicative of future results.

Information obtained from third party sources are believed to be reliable but not guaranteed. Envestnet|PMC™ makes no representation regarding the accuracy or completeness of information provided herein. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice.

Investments in smaller companies carry greater risk than is customarily associated with larger companies for various reasons such as volatility of earnings and prospects, higher failure rates, and limited markets, product lines or financial resources. Investing overseas involves special risks, including the volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. Income (bond) securities are subject to interest rate risk, which is the risk that debt securities in a portfolio will decline in value because of increases in market interest rates. Exchange Traded Funds (ETFs) are subject to risks similar to those of stocks, such as market risk. Investing in ETFs may bear indirect fees and expenses charged by ETFs in addition to its direct fees and expenses, as well as indirectly bearing the principal risks of those ETFs. ETFs may trade at a discount to their net asset value and are subject to the market fluctuations of their underlying investments. Investing in commodities can be volatile and can suffer from periods of prolonged decline in value and may not be suitable for all investors. Index Performance is presented for illustrative purposes only and does not represent the performance of any specific investment product or portfolio. An investment cannot be made directly into an index.

Alternative Investments may have complex terms and features that are not easily understood and are not suitable for all investors. You should conduct your own due diligence to ensure you understand the features of the product before investing. Alternative investment strategies may employ a variety of hedging techniques and non-traditional instruments such as inverse and leveraged products. Certain hedging techniques include matched combinations that neutralize or offset individual risks such as merger arbitrage, long/short equity, convertible bond arbitrage and fixed-income arbitrage. Leveraged products are those that employ financial derivatives and debt to try to achieve a multiple (for example two or three times) of the return or inverse return of a stated index or benchmark over the course of a single day. Inverse products utilize short selling, derivatives trading, and other leveraged investment techniques, such as futures trading to achieve their objectives, mainly to track the inverse of their benchmarks. As with all investments, there is no assurance that any investment strategies will achieve their objectives or protect against losses.

Neither Envestnet, Envestnet|PMC™ nor its representatives render tax, accounting or legal advice. Any tax statements contained herein are not intended or written to be used, and cannot be used, for the purpose of avoiding U.S. federal, state, or local tax penalties. Taxpayers should always seek advice based on their own particular circumstances from an independent tax advisor.

© 2014 Envestnet. All rights reserved.